In the fast-moving world of semiconductors, even small portfolio shifts by industry giants can send powerful signals. Taiwan Semiconductor Manufacturing Company Limited (TSM), the world’s largest chip foundry, has now fully exited its investment in Arm Holdings plc (ARM).

In a filing this week, TSMC confirmed it has sold its remaining stake in Arm of about 1.1 million shares for roughly $231 million, completing a divestment that began after Arm’s 2023 IPO. The move effectively unwinds what was once a strategic investment in one of the most critical chip architecture players in the artificial intelligence (AI) era.

Despite the headline exit, Arm shares were still modestly higher in Wednesday trading, suggesting investors aren’t reading this as a loss of confidence or a threat to the company’s long-term narrative, at least not yet.

So, if one of the most sophisticated players in the chip ecosystem has decided to cash out, should you follow, or is this simply smart portfolio management that doesn’t change Arm’s growth story?

About Arm Holdings Stock

Arm Holdings is a semiconductor and software design company best known for developing the ARM architecture, a family of energy-efficient central processing unit designs widely licensed across the technology industry. Headquartered in the United Kingdom, Arm doesn’t manufacture physical chips itself but instead generates revenue by licensing its processor designs and related intellectual property to semiconductor companies and original equipment manufacturers, while also earning royalties on chips shipped by its partners. Arm went public on the NASDAQ in September 2023, and its market cap is around $222 billion.

Arm Holdings stock has delivered one of the most explosive runs in the semiconductor space, driven largely by investor enthusiasm around AI, custom silicon, and its expanding role in data centers.

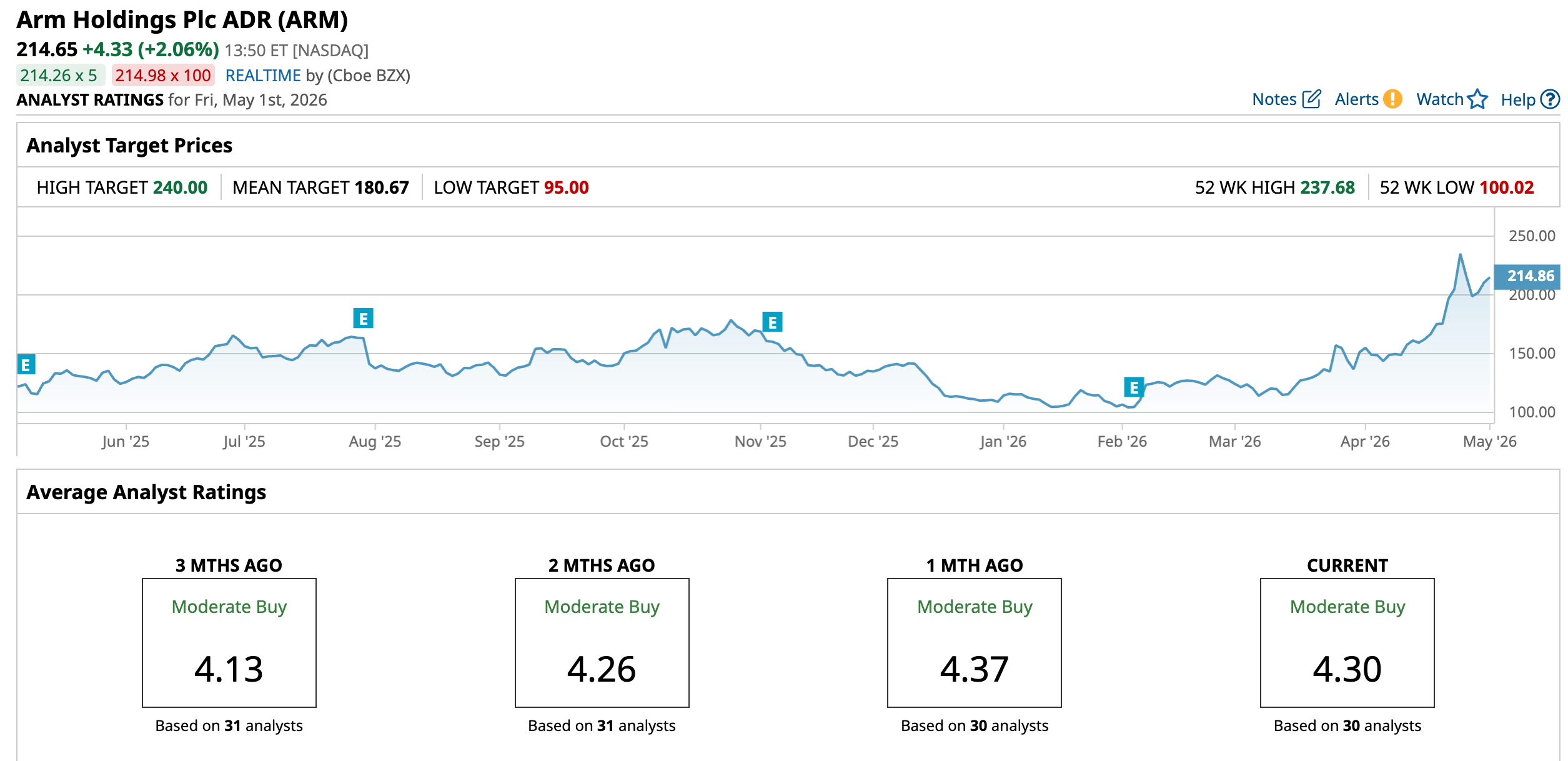

Over the past 52 weeks, the stock has surged sharply, with returns of 85.3%. This places Arm among the top-performing large-cap semiconductor names during the AI-driven rally.

The momentum has been even more striking year-to-date (YTD), where the stock is up 95.62%. The rally has been fueled by strong earnings, rising royalty streams, and growing expectations that Arm will capture a larger share of AI compute economics.

Moreover, Arm Holdings’ recent rally culminated in a sharp breakout on April 24, when the stock surged 14.76% intraday to a 52-week high of $237.68. The move was sparked in part by a broad semiconductor rally following strong results from Intel Corporation (INTC), which reinforced the narrative that agentic AI is accelerating demand for CPUs, directly benefiting Arm’s architecture ecosystem.

Also, investors responded to ARM’s unveiling of a new AI-focused CPU and its push into custom silicon, and potential long-term AI data center growth. These factors created a near-perfect setup for a breakout, sending the stock to record levels and it remained largely unaffected by the recent selloff by Taiwan Semi.

The stock is trading at a significant premium compared to industry peers at 168.35 times forward earnings.

Better-than-Expected Quarterly Performance

Arm Holdings reported its fiscal third-quarter 2026 results on Feb. 4 (for the quarter ended Dec. 31, 2025), delivering another strong set of numbers that underscored its growing role in AI-driven computing.

The company posted revenue of $1.2 billion, up 26% year-over-year (YOY), marking its fourth consecutive billion-dollar quarter, while adjusted EPS came in at $0.43, rising about 10.3% YOY, both exceeding Wall Street expectations.

Royalty revenue, the key profit driver, climbed 27% YOY to $737 million, benefiting from increasing adoption of Armv9 architectures and higher royalty rates per chip, particularly in data center and AI workloads, while licensing revenue rose 25% YOY to $505 million as demand for next-generation designs remained robust. Its Annualized contract value (ACV) increased 28% YOY.

Furthermore, for fiscal Q4, management is projecting revenue of around $1.47 billion +/- $50 million and adjusted EPS of approximately $0.58 +/- $0.04.

The outlook reflects sustained strength in AI-related demand across cloud, edge, and mobile markets.

Analysts predict EPS to be around $0.85 for fiscal 2026, a decline of around 19.8% YOY, but again rise 38.8% to $1.18 in fiscal 2027.

What Do Analysts Expect for Arm Stock?

Recently, Wells Fargo raised its price target on Arm to $220 from $175 and maintained an “Overweight” rating, citing strong long-term AI-driven growth prospects.

On the other hand, Morgan Stanley downgraded Arm to “Equal Weight” from “Overweight” while raising its price target to $150. The firm highlighted Arm’s strategic shift into chipmaking and its positioning for agentic AI as long-term positives, but cautioned that commercialization will take time.

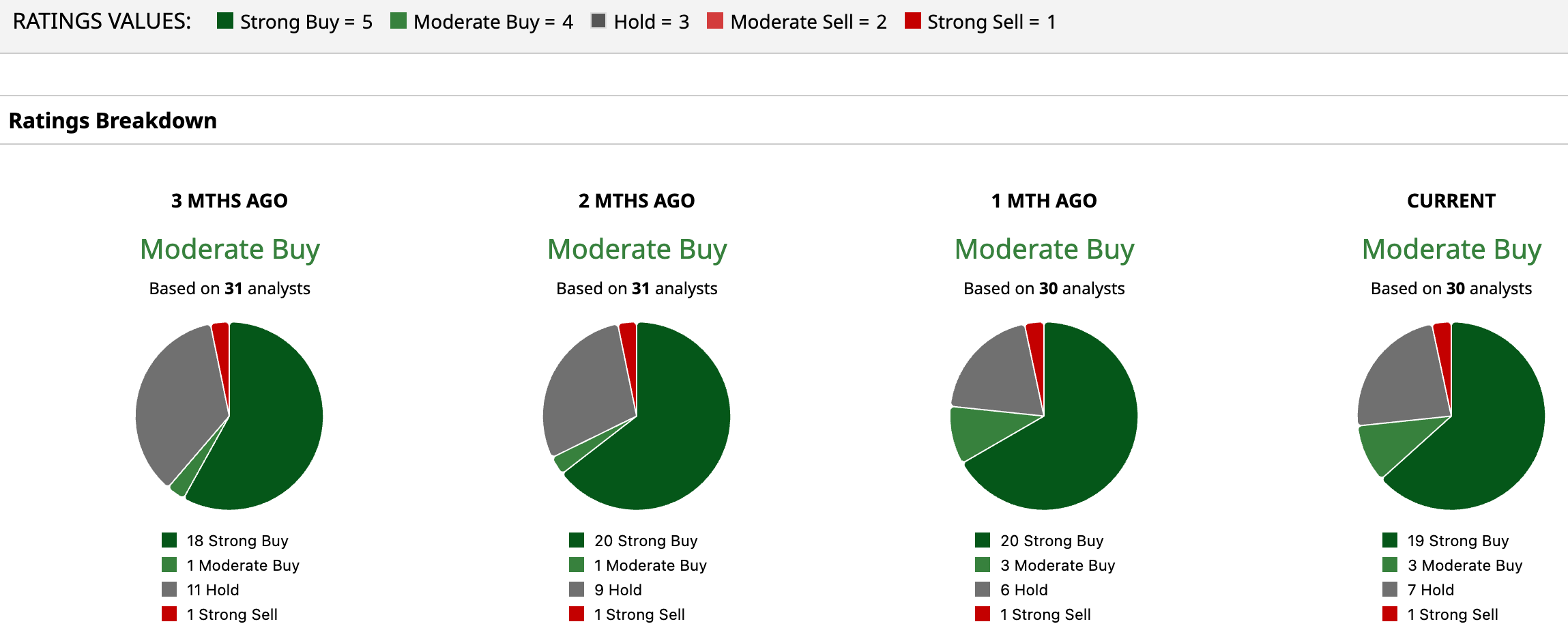

The stock has a consensus “Moderate Buy” rating overall. Out of 30 analysts covering the stock, 19 recommend a “Strong Buy,” three give a “Moderate Buy,” seven analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

ARM has already surged past its average analyst price target of $180.67, while the Street-high target price of $240 suggests 11.8% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- These Are April's 2 Hottest AI Stocks. Should You Buy Them in May?

- Google Just Warned of a Significant Increase in 2027 CapEx. Why GOOGL Stock Investors Don’t Seem to Care.

- Taiwan Semi Is Selling ARM Stock. Should You?

- McDonald’s Is Down 4% and Starbucks Is Up 25% in 2026. The Better Dividend Stock Might Surprise You.